The

failed EDF nuke project at Calvert Cliffs in Maryland

makes it clearer why Southern Company (SO) was the first company

to get a nuclear permit in 30 years:

it was the only one big enough and monopolistic enough to pull it off.

Even then it’s such a

bet-the-farm risk

that even

“great, big company”

SO only dared

to deploy its

“great big huge scale“ equipment

with the regulatory capture triple-whammy

of

a stealth tax on Georgia Power bills,

PSC approval of cost overruns,

and

an $8.33 billion federal loan guarantee:

The

failed EDF nuke project at Calvert Cliffs in Maryland

makes it clearer why Southern Company (SO) was the first company

to get a nuclear permit in 30 years:

it was the only one big enough and monopolistic enough to pull it off.

Even then it’s such a

bet-the-farm risk

that even

“great, big company”

SO only dared

to deploy its

“great big huge scale“ equipment

with the regulatory capture triple-whammy

of

a stealth tax on Georgia Power bills,

PSC approval of cost overruns,

and

an $8.33 billion federal loan guarantee:

-

a legislated

stealth tax in the form of

a rate hike on Georgia Power customers for

power they won’t get for years if ever.

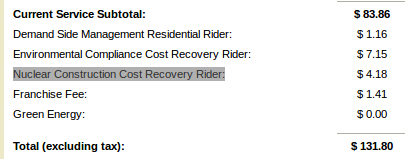

If you’re a Georgia Power customer,

look on your bill for Nuclear Construct Cost Recovery Rider.

You’ll find it adds about 5% on top of your Current Service Subtotal.

Georgia is one of only a handful of states where such a

Construction Work in Progress (CWIP) charge is legal

thanks to our regulatory-captured legislature.

Doubling down on bad energy bets,

Southern Company is also

trying to use CWIP to build a coal plant in Mississippi.

a legislated

stealth tax in the form of

a rate hike on Georgia Power customers for

power they won’t get for years if ever.

If you’re a Georgia Power customer,

look on your bill for Nuclear Construct Cost Recovery Rider.

You’ll find it adds about 5% on top of your Current Service Subtotal.

Georgia is one of only a handful of states where such a

Construction Work in Progress (CWIP) charge is legal

thanks to our regulatory-captured legislature.

Doubling down on bad energy bets,

Southern Company is also

trying to use CWIP to build a coal plant in Mississippi.

-

A captive Public Service Commission that

rubber-stamps costs for Plant Vogtle.

In case there was any doubt as to the PSC’s role in legitimizing those new nukes,

the very next day Fitch reaffirmed Southern Company’s bond ratings.

A captive Public Service Commission that

rubber-stamps costs for Plant Vogtle.

In case there was any doubt as to the PSC’s role in legitimizing those new nukes,

the very next day Fitch reaffirmed Southern Company’s bond ratings.

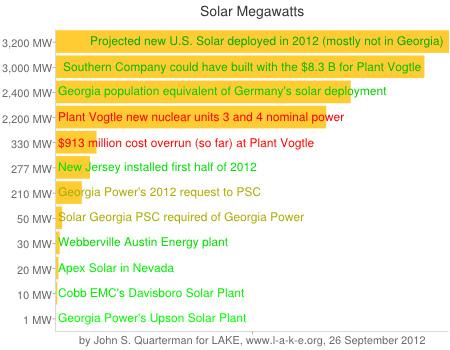

Translation: Georgia Power customers subsidize SO’s bonds and SO shareholders’ stock dividends. The PSC also approved cost overruns being passed on to Georgia Power customers, and those nukes are already over $400 or $900 million, depending on who you ask. What do you expect when 4 out of 5 Public Service Commissioners apparently took 70% of their campaign contributions from utilities they regulate or their employees or their law firms, and the fifth commissioner took about 20% from such sources? Hm, there’s an election going on right now!Southern Company’s regulated utility subsidiaries derive predictable cash flows from low-risk utility businesses, enjoy relatively favorable regulatory framework in their service territories, and exhibit limited commodity price risks due to the ability to recover fuel and purchased power through separate cost trackers.

-

An

$8.33 billion federal loan guarantee.

Even that’s not good enough for SO and Georgia Power: SO is

asking for less down payment.

An

$8.33 billion federal loan guarantee.

Even that’s not good enough for SO and Georgia Power: SO is

asking for less down payment.

And what if even one of that three-legged regulatory capture stool’s legs went away? Continue reading