A writer for Forbes spells out the question of nuclear investment: how can something that expensive, over-budget, late, and phenomenally risky be a good investment, especially when cheaper and faster energy sources are readily available?

Peter Kelly-Detwiler wrote for Forbes today, New Centralized Nuclear Plants: Still an Investment Worth Making?

Just a few years ago, the US nuclear renaissance seemed at hand. It probably shouldn’t have been. Cost overruns from Finland to France to the US were already becoming manifest, government guarantees were in doubt, and shale gas drillers were beginning to punch holes into the ground with abandon.

Then came Fukushima. The latter proved a somewhat astonishing reminder of forgotten lessons about nuclear power risks, unique to that technology: A failure of one power plant in an isolated

location can create a contagion in countries far away, and even where somewhat different variants of that technology are in use. Just as Three Mile Island put the kaibosh on nuclear power in the US for decades, Fukushima appears to have done the same for Japan and Germany, at a minimum. It certainly did not help public opinion, and at a minimum, the effect of Fukushima will likely be to increase permitting and associated regulatory costs.

He goes into detail: they take too long (while gas and solar got cheaper), they’re extremely expensive to build and run, and they’re all-or-nothing investments.

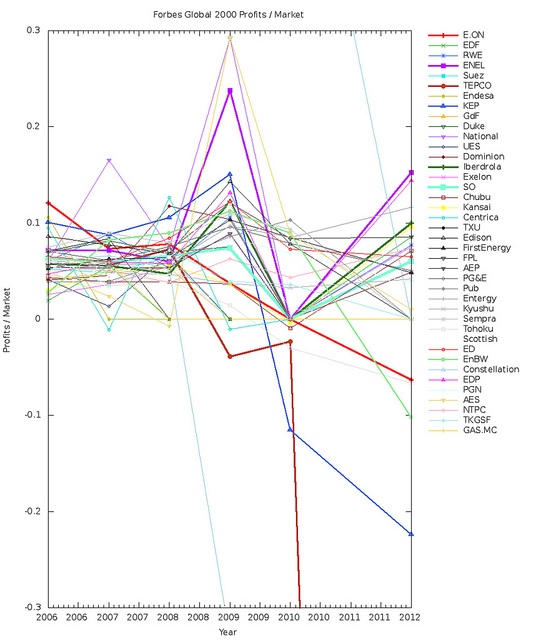

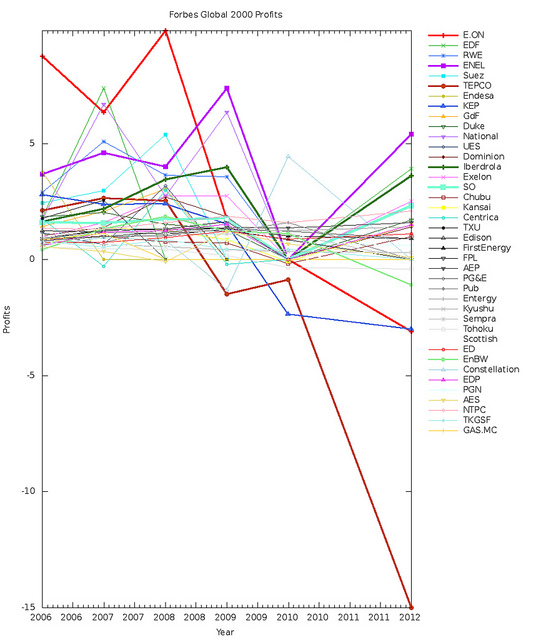

I was going to compile this list of recent nuclear financial failures, but he saves us all the trouble:

Continue reading