Road trip to Callaway Gardens for the annual question time with Tom Fanning, questions provided by environmentalists and Southern Company (SO) stockholders from at least four states.

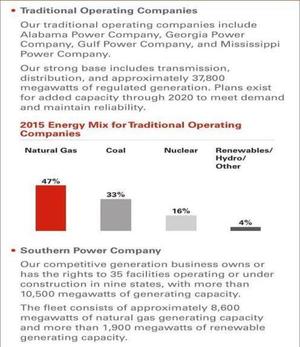

This figure from page ii of the meeting Notice illustrates both the problem and the solution for Southern Company.

Natural gas has replaced coal as SO’s top energy source, and Nuclear is still

in there.

But renewables are up to 4%.

And over on the right of the same page:

This figure from page ii of the meeting Notice illustrates both the problem and the solution for Southern Company.

Natural gas has replaced coal as SO’s top energy source, and Nuclear is still

in there.

But renewables are up to 4%.

And over on the right of the same page:

- Growth in Renewables

Approximately 3,800 megawatts of announced or added renewable capacity since 2012. This includes the development of what is expected to be the largest voluntary solar portfolio in the U.S. (at Georgia Power Company).

Interesting use of “voluntary”, but never mind that. If SO keeps that up, it will be more than doubling its solar capacity every two years, faster than the national average. And that 4% will in less than ten years become the majority energy source.

Here are the materials provided for the meeting:

- Notice of 2016 Annual Meeting of Stockholders and Proxy Statement

- Southern Company 2015 Annual Report

Here, from where they were hidden on page 88, are the two stockholder proposals the board recommends voting against, on the IEA’s 2 degree scenario and on coal as stranded assets. SO didn’t say for either one who proposed them.

Item 9

REPORT ON STRATEGY FOR INTERNATIONAL ENERGY AGENCY 2°C SCENARIO

Whereas:

The 2014 Intergovernmental Panel on Climate Change (IPCC) Synthesis Report warns that global warming will have “severe, pervasive and irreversible impacts for people and ecosystems.” The costs of failing to address climate change are significant and are estimated to have an average value at risk of $4.2 trillion globally. To mitigate the worst impacts of climate change and limit warming to below 2 degrees Centigrade (2°C), as agreed in the Cancun Agreement, the IPCC estimates that a fifty percent reduction in greenhouse gas (GHG) emissions globally is needed by 2050, relative to 1990 levels.

The Southern Company has had a proactive response toward the low-carbon transition by adding more than 3,600 MW of renewable projects since 2012, developing ‘clean coal’ technology, adding nuclear energy generation, and making the first offer by a utility for investment-grade Green Bonds valued at $1 billion.

However, accelerated efforts are necessary: Southern is the third largest Carbon Dioxide (C0 2 ) emitter in the country and ranked 26th out of 32 utility companies for Energy Efficiency Savings in a benchmarking report produced by Ceres in 2014.

Regulatory and technology changes are underway that will profoundly impact the utility business model. The U.S. Environmental Protection Agency (EPA) recently finalized the Clean Power Plan, requiring states to achieve 32% GHG reductions on average nationwide (from 2005 levels). Yet the International Energy Agency (lEA) 2°C Scenario requires a 90% reduction of global average carbon intensity of electricity production by 2050, necessitating significant action beyond the Clean Power Plan. Meanwhile, developments in new technologies are leading to sharply declining costs, increasing competitiveness of renewable energy generation and storage.

Rates must be designed for maximum flexibility to achieve climate objectives while providing just and universal access to electricity services, including affordable services to low-income customers.

Recognizing the unique constraints on innovation for the low-carbon transition in each regulated market, Southern’s subsidiary companies can demonstrate a willingness to work with regulators to develop frameworks to catalyze the low-carbon transition. In Minnesota, utilities, rate-payers, and regulators are collaborating to map the transition to a regulatory model that enables innovation, customer options, and realizes public policy goals.

Proponents offer this supportive but stretching resolution to urge Southern to position itself to thrive for the long-term in a decarbonized energy sector.

RESOLVED: Shareholders request that Southern Company issue a report by November 30, 2016, at reasonable cost and omitting proprietary information, on Southern’s strategy for aligning business operations with the IEA 2°C scenario, while maintaining the provision of safe, affordable, reliable energy.

Supporting Statement:

Proponents believe this report may include:

- Plans to integrate technological, regulatory, and business model innovations such as: distributed energy resources (storage and generation), demand response, smart grid technologies, and increased customer energy efficiency, as well as corresponding revenue models and rate designs.

- Information on aligning incentives, research and development, public policy positions, engagement strategy with state regulators, and board governance with Southern’s business plan compatible with this strategy.

The Board’s Statement of Opposition basically says both they’re already doing that and they don’t need to do that.

Item 10

REPORT QUANTIFYING POTENTIAL FINANCIAL LOSSES TO THE COMPANY ASSOCIATED WITH STRANDING OF COAL ASSETS

Whereas:

The Southeast’s economic growth “is at risk from unchecked climate change, which could render this region— already one of the hottest and most weather vulnerable of the country— at significant economic risk.” (Risky Business, 2015).

Because coal causes 77% of U.S. energy related emissions, regulations designed to halt or mitigate climate change will likely target coal. (EPA, Electricity Sector Emissions, 2014). This may lead to stranding— premature write downs, or devaluations of coal assets. For instance, in 2015, the U.S. finalized the Clean Power Plan, which requires the electric power sector to significantly reduce carbon emissions. HSBC noted that the rules could “increase the stranding risk for U.S. coal producers and coal heavy utilities.” Coal fired utilities claimed that the regulations will “result in billions of dollars in stranded assets.” (Comment to EPA from Coalition for Innovative Climate Solutions).

In contrast to peers, Southern Company is making big bets on carbon capture and storage (“CCS”) and coal gasification, with the hope of trapping carbon pollution and storing it indefinitely, similar to nuclear waste. However, there is tremendous controversy and conflicting data on whether CCS works, is cost effective, and can overcome high water requirements, and other challenges. Coal gasification attempts to reduce coal’s carbon intensity by converting coal to gas, then burning it. Coal gasification is not widely employed because natural gas is a less expensive alternative that achieves similar carbon savings. Southern Company’s Kemper coal gasification plant is nearly $4 billion dollars over-budget and two years delayed, resulting in Southern’s subsidiary, Mississippi Power, having its credit downgraded. Mississippi has also not committed to full cost recovery for Kemper, and the state Supreme Court refunded Kemper-related costs to customers.

Southern’s emphasis on CCS and coal gasification constitute a gamble that may increase, rather than reduce, its carbon asset risk. Southern’s focus on these technologies discourages the Company from shuttering or converting coal plants, exposing investors to billions of dollars of risk due to uncertainty about technical viability and cost effectiveness. Kemper has already resulted in millions of dollars of losses being born by shareholders.

THEREFORE BE IT RESOLVED:

Shareholders request that Southern Company prepare a report by September 2016, omitting proprietary information and at reasonable cost, quantifying potential financial losses to the company associated with stranding of its coal assets under a range of scenarios for climate change driven regulations that mandate greenhouse gas reductions beyond those required by the Clean Power Plan. Such report should include possible financial losses if coal gasification and/or CCS is rejected by policymakers as a technical climate mitigation strategy, or if they cannot be cost effectively implemented. Shareholders also request that Southern disclose, in the report, its total investments in CCS and coal gasification technologies.

I’ll quote this first point from the Board’s rebuttal:

- Preparing a report on the financial impact to the Company of regulations that would require GHG reduction beyond the Clean Power Plan is impractical, given the significant uncertainty around the content, timing, and stringency of rules that have not yet been proposed. Additional uncertainty results from the potential impact of future regulatory decisions on the Southern Company system’s proposed asset retirements and related cost recovery. As a result, any conclusions in such a report, if prepared, would be so speculative as to be of little value to investors.

So SO admits it doesn’t know that Kemper Coal will actually work. What say we call off Kemper Coal and the Plant Vogtle nuke boondoggle and get on with solar power?

-jsq

Short Link: